CSRD, ESG and Sustainability

Environmental, Social, and Governance (ESG) Reporting

Environmental, Social, and Governance (ESG) Reporting have increasingly become more and more important for companies. However not all aspects of E, S and G are equally important for all companies. When an organisation determines the various dimensions of ESG where it was to be excellent and where it wants to be good, important decisions have to be made.

Considering ESG requires consideration of the needs and expectations of a range of interested parties or stakeholders. Expectations are shifting over time and can hugely impact business dynamics. Business value and impact are not equal to financial performance. As such companies have to consider the broader perspective including development of a core strategy in combination with risks and opportunities, growth and creating long-term value.

Mapping for ESG requires a thorough exercise performed through different steps. Quite often it is a learning path. A successful way is to build a roadmap and framework that sets out the ambitions, goals and milestones. A roadmap for implementation, target setting, milestones and rationale will create buy-in from stakeholders, employees, public and investors. A roadmap incorporates being accountable for critical initiatives.

A materiality assessment will help understand your internal and external stakeholders priorities and relevance of ESG topics from their perspective. Once this step taken, it is important to assess the current status on existing programs, policies; metrics and engagements. Once the baseline is clear, define clear objectives and targets. Define a strategic roadmap to reach those ambitions. And finally report your progress.

Corporate Sustainability Reporting Directive (CSRD)

Welcome to the future of sustainability reporting. The European Union’s Corporate Sustainability Reporting Directive (CSRD) and European Sustainability Reporting Standards (ESRS) are set to revolutionize the way businesses report on their social and environmental impacts.

Understanding CSRD and ESRS

The CSRD and ESRS are comprehensive frameworks that require companies to provide detailed reports on their sustainability performance. These reports must cover a wide range of topics, including environmental impacts, social issues, human rights, governance factors, and more.

Who Needs to Comply?

The CSRD applies to all large EU companies, most businesses with operations or securities in Europe, including small and medium-sized enterprises (SMEs), and non-EU parent companies with a cumulative group turnover in the EU greater than €150 million. If an undertaking meets 2 of 3 criteria below, it is considered ‘large’:

more than 250 FTE

more than 50 mio euro turn-over

more than 25 mio euro balance sheet total

This means that nearly 40-50,000 companies across the European Economic Area will need to comply.

Key Dates to Remember

The timeline for compliance varies depending on the size of your company:

Large EU companies with over 500 employees: Start data collection in January 2024 for reporting in 2025.

Other large EU companies: Start data collection in January 2025 for reporting in 2026.

SMEs listed on an EU regulated market: Start from 1 January 2026 for FY 2026 with reports due in 2027.

Companies with a significant presence in the EU but whose ultimate parent company is outside the EU: Start from 1 January 2028 for FY 2028 with reports due in 2029.

Reporting Requirements for Companies:

Business Strategy and Sustainability: Provide detailed information and data about your business strategy, highlighting sustainability-related opportunities.

Sustainability Targets: Outline your sustainability targets and the measures in place to control and achieve them.

Greenhouse Gas Emissions: State your goals for reducing greenhouse gas emissions.

Global Warming Mitigation: Present your plans to support the global effort to limit warming to 1.5°C.

Environmental Impact Prevention: Describe the actions taken to prevent any identified environmental impacts.

Compliance: Ensure adherence to all relevant regulations.

Non-Compliance Penalties:

Public Disclosure: Companies must publicly disclose any infringements, including naming the responsible individuals.

Cessation Orders: Orders to cease activities in the area of infringement.

Financial Penalties: Fines proportional to the company’s profits.

Preparing for Compliance

Compliance with the CSRD and ESRS requires a comprehensive approach to sustainability reporting. Companies will need to provide detailed information on a wide range of topics, publish this information in a dedicated section of their annual report, and extend their disclosures to include their entire value chain. The concept of ‘double materiality’ is also crucial. This means that companies must report on both their impacts on the environment and the climate-related risks they face.

Navigating these new requirements can be challenging, but you don’t have to do it alone. Our team of experts is here to guide you through every step of the process. Contact us today to learn more about how we can help your business comply with the CSRD and ESRS and become a leader in sustainability.

Why Choose Us?

Experience and Expertise: With years of experience in the field, our team has the knowledge and skills to help your business navigate the complexities of CSRD. We understand the unique challenges and opportunities that come with integrating sustainability into business operations.

Customized Solutions: We believe that every organization is unique. That’s why we offer tailored solutions that fit your specific needs and objectives. We work closely with you to understand your business and develop a CSRD strategy that aligns with your goals.

Result-Oriented Approach: Our focus is on delivering tangible results. We help you implement effective CSRD initiatives that not only benefit society and the environment, but also contribute to your bottom line

Our Services

CSRD Strategy Development: We help you develop a comprehensive CSRD strategy that aligns with your business objectives and stakeholder expectations.

Sustainability Reporting: We assist you in creating transparent and credible sustainability reports that meet international standards and best practices.

Stakeholder Engagement: We guide you in engaging effectively with your stakeholders, helping you build strong relationships and trust.

Training and Capacity Building: We offer training programs to equip your team with the necessary skills and knowledge to implement your CSRD strategy effectively.

-

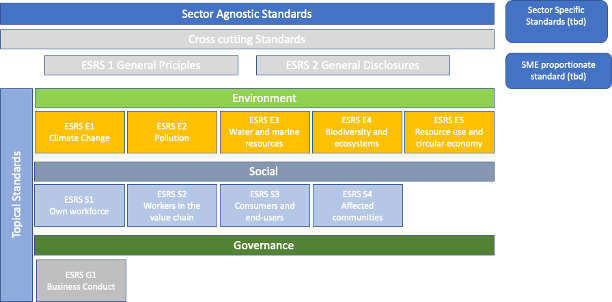

Environmental

Environmental categories include:

Climate change

Pollution

Water and marine resources

Biodiversity and ecosystems

Resource use and circular economy

-

Social

Social categories include:

The company’s own workforce

Workers in the value chain

Affected communities

Consumers and end users

-

Governance

Governance categories include:

Governance

Risk management and internal control

Business conduct